Our approach to tax

Taxation is an important issue for us and our stakeholders, including our shareholders, governments, customers, suppliers, employees and the global communities in which we operate.

Our tax strategy1 is to conduct and manage our tax affairs in accordance with our tax principles. Our tax principles are aligned with the Group’s wider business philosophy and values as detailed in our Code of Ethics and Business Conduct. We present our strategy to, and receive approval from, our Audit Committee each year. We periodically discuss our tax principles with a variety of external stakeholders and we update our approach to tax and tax principles on an annual basis.

Objectives for the tax department against which their performance is measured are as follows:

- To support the Group’s commercial activity by working closely with the business units

- To comply with all tax-related obligations

- To manage the Group’s tax risk and reputation

- To maintain a predictable and sustainable tax rate

Corporate responsibility and sustainability (ESG) are foundational to RELX and play an important role in our approach to tax:

- Governance: RELX is a responsible taxpayer. We are transparent about our approach to tax and we publish our tax principles, tax risk management, tax risk control framework and our total tax contribution below.

- Social: Our unique contributions to society are at the heart of our business as illustrated by the tax related case studies in the ‘unique contributions to society’ section below. We are also committed to doing our part to advance the UN’s sustainable development goals, specifically SDG 16 (Peace, Justice and Strong Institutions) by promoting the rule of law in the tax arena.

- Environmental: RELX does not pay material amounts of environmental taxes as our own operations do not have a significant environmental impact, however we support our employees with reducing their environmental impact through tax incentivised programmes encouraged by governments, for example for the adoption of zero or low emission modes of transport such as bicycles or electric vehicles.

1 We welcome the UK government’s requirement for large businesses to publish their UK tax strategy. Our UK tax strategy is incorporated within our global tax strategy and tax principles and we regard the publication of this information as complying with the duty under the UK’s Finance Act 2016, Schedule 19, para 16 for the financial year ending 31 December 2026.

Our tax principles

These tax principles apply to all taxes in all countries. Furthermore, these principles apply to all individuals involved in managing or directing RELX's tax affairs.

1. Accountability and governance

The Board receives, through its Audit Committee, regular updates on material tax issues, tax disputes, effective tax rates and any changes to the tax strategy. Updates are provided to the Board by the Chief Financial Officer (CFO). We report annually to our Audit Committee on adherence to our tax principles. This includes an assessment of how our tax strategy and tax principles are aligned with the Group’s wider business strategy and values. Each year, our CFO and other finance representatives sign off the Senior Accounting Officer obligations in the UK. In addition, the Board monitors the company’s risk management and internal control systems and annually carries out a review of their effectiveness and reports on that review in the annual report. The review includes consideration of how tax risks are managed, monitored and assured.

The tax affairs of RELX are managed by a team of suitably qualified tax professionals, supported where appropriate by external advisors. Training is provided to employees to ensure that tax compliance is carried out with a suitable level of diligence and technical expertise.

2. Relationship with governments

RELX actively engages with policymakers, tax administrators, industry bodies and international institutions. In addition, we participate in consultations with the Organisation for Economic Co-operation and Development (OECD), European bodies and the United Nations. We support the approach of the OECD Framework for formal co-operative compliance regimes.

We respect the rights of governments to determine their own tax regimes, rates of tax and collection mechanisms.

3. Relationships with tax authorities

We maintain professional working relationships with taxing authorities around the world:

- We are open and transparent about our tax affairs and significant transactions.

- We work co-operatively to resolve issues in a positive and professional manner.

We support co-operative compliance and related programmes where they are available; we are part of the top 100 largest taxpayers programme in the Netherlands and proactively engage with tax authorities such as with HMRC in the UK business risk review.

4. Compliance

We aim to comply with laws and regulations in all the countries in which we have a taxable presence, taking into account not only the letter but also, where clearly discernible, the spirit of the law. We make full and timely disclosures in tax returns, reports and documents submitted to taxing authorities.

We do not accept or tolerate the criminal evasion of any tax in any jurisdiction, or the deliberate and dishonest facilitation of another’s tax evasion, whether carried out by an employee or any other associated business partner acting for us or on our behalf. We will not conduct business with anyone we believe is engaging in such practices in any jurisdiction.

We prepare and maintain all documentation required by law, as well as anywhere necessary to provide support for a transaction with a tax impact.

We use tax technology to improve the efficiency and robustness of our tax processes and tax data management. We regularly review and enhance our systems and processes supporting both direct and indirect taxes.

5. Transfer pricing

We do not artificially transfer profits from one business location to another to avoid taxation. We aim to pay an appropriate amount of tax according to where value is created within the normal course of commercial activity.

Cross-border transactions undertaken between Group subsidiaries are taxed on an ‘arm’s-length’ basis in accordance with the principles endorsed by the OECD and the United Nations Committee of Experts on International Cooperation in Tax Matters.

6. Transparency

We comply with all current tax transparency requirements, and support international efforts to provide meaningful insight to stakeholders by publishing information in addition to the minima required by existing law and accounting standards.

7. Business structure

In making commercial decisions we take tax into account in the same way as any other cost. Where there is more than one way of structuring a commercial business arrangement we will take a holistic view, considering all factors including tax. We may implement an alternative with a lower tax cost, provided it is compliant with the laws and relevant regulations in the jurisdictions concerned and on the basis that we will make full and timely disclosures to the affected jurisdictions.

We will not enter into tax planning, transactions or structures

(i) that are notifiable to tax authorities under mandatory disclosure regimes which apply where obtaining a tax advantage is the main benefit or one of the main benefits of the arrangement,

(ii) which we consider to be abusive, or

(iii) which otherwise have no ultimate commercial business purpose.

8. Tax havens

We do not use companies in tax havens as defined by the OECD to avoid taxes on activities which take place elsewhere.

9. Uncertainty and risk

We adopt a prudent approach to tax risk and seek to achieve an acceptable risk level in all activities, taking into consideration financial risks, relationships with tax authorities and the reputation of the group. We use standard processes and procedures to assess tax risk before a significant transaction is undertaken and to monitor the position until final resolution. In considering tax risk associated with such a transaction we assess:

- If it is aligned to the Tax Principles

- Internal and/or external advice from suitably qualified advisors

- Whether the tax treatment applied is more likely than not to be sustained on examination by tax authorities

Training is provided to relevant employees to ensure that tax risk assessment processes are followed appropriately, and mechanisms are in place to allow employees to raise concerns around application of these principles in general or to specific transactions, in line with the RELX Code of Ethics and Business Conduct and the RELX Reporting Concerns policy. Our in-house Internal Audit and Assurance team periodically review these processes and procedures to ensure that they remain sufficient and appropriate.

10. Tax incentives and rulings

We do not use our commercial bargaining power in any given country or region to obtain company-specific tax advantages that are not available to all market participants, or which are otherwise not properly legislated.

Tax Risk management

Our businesses operate globally, and our profits are subject to taxation in many different jurisdictions and at different tax rates. As a result of various local and international initiatives, tax laws that currently apply to our businesses may be amended by the relevant authorities or interpreted differently by them and this creates added uncertainty.

The risks are managed through our Tax Risk Framework, which sets out the key tax risks and the mitigating actions that RELX takes to manage and monitor those risks. There are five key risk areas covered by the tax risk framework – policy & governance; organisation and resources; compliance and documentation; external tax reporting and communications; and change management. Examples of a risk and mitigating action for each of the five key risk areas are shown below:

Tax Risk Control Framework

Our global tax contribution

RELX contributes in many ways to the jurisdictions in which we operate. This report concentrates on our tax contribution which is just one element of our overall contribution. Total tax contribution quantifies the total amount of taxes generated by RELX and contributed to the public finances.

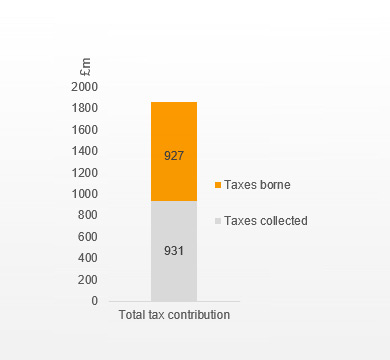

For many of the markets in which we operate our tax contribution is significant. In the year ended 31 December 2025, our total tax contribution, including both our own taxes and those we collect on behalf of governments, was £1,858m. These are cash taxes generated directly by our economic activity in each country and are a fair reflection of our tax footprint and what we contribute to government tax revenues.

Total tax contribution for 2025

We pay taxes where our economic activity takes place, with the US, UK and the Netherlands being our largest jurisdictions. Taxes borne of £927m in 2025 are those that represent a cost to us. This amount includes corporate tax, employer payroll taxes, property, and indirect taxes. Taxes collected of £931m in 2025 are those that we administer on behalf of governments and collect from others as we do business. This amount includes employee taxes, net VAT and sales taxes collected.

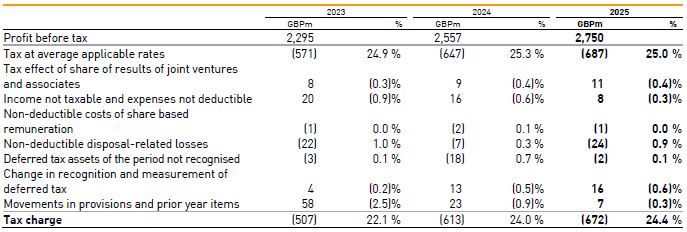

More detail on the corporate income taxes reflected in our annual accounts can be found in note 9 of RELX’s 2025 annual report. The reconciliation of our effective tax rate to the weighted average expected rate is reproduced below.

The weighted average applicable tax rate for the year was 25.0% (2024: 25.3%; 2023: 24.9%), reflecting the applicable rates in the countries where the Group operates. The Group’s future tax charge will be sensitive to the geographic mix of profits and losses and the tax rates and laws in force in the jurisdictions in which the Group operates.

The BEPS Pillar Two Minimum Tax legislation was enacted in July 2023 in the UK with effect from 2024. The Group has applied the temporary exception under IAS 12 in relation to the accounting for deferred taxes arising from the implementation of the Pillar Two rules. The rules, including the Side-by-Side agreement released by the OECD in January 2026, do not have a significant impact on the tax charge for the Group.

Other international tax developments, including in the US, do not have any significant impact on the Group.

The effective tax rate of 24.4% (2024: 24.0%; 2023: 22.1%) was lower than the weighted average applicable rate of 25.0%. Income not taxable and expenses not deductible include research and development and other tax credits of £20m (2024: £21m; 2023: £21m). In 2023, there were tax credits arising from the substantial resolution of prior year tax matters.

Our unique contributions to society

RELX performs to the highest commercial and ethical standards and channels our knowledge and strengths, as global leaders in our industries, to make a difference to society. We make a positive impact on society through our knowledge, resources and skills, including supporting the tax authorities and promoting of the rule of law and justice.

Case studies

LexisNexis Homestead Exemption Fraud Detection Solution

Residential property tax fraud, also called homestead exemption fraud, occurs in US counties when taxpayers wrongly receive residential property tax breaks on homes they don’t live in as their primary residence or receive tax exemptions for which they otherwise don’t qualify, such as those for senior citizens. This type of fraud costs US counties millions each year, which has a significant impact on funding for public services, including schools, public safety and other local needs.

Residential property tax fraud, also called homestead exemption fraud, occurs in US counties when taxpayers wrongly receive residential property tax breaks on homes they don’t live in as their primary residence or receive tax exemptions for which they otherwise don’t qualify, such as those for senior citizens. This type of fraud costs US counties millions each year, which has a significant impact on funding for public services, including schools, public safety and other local needs.

In the state of Illinois, the Cook County Assessor’s Office needed an investigative tool to help detect these fraudulent tax filings, so it implemented the LexisNexis Homestead Exemption Fraud Detection Solution. Powered by HPCC Systems, the solution examines the homestead exemption filings of the county’s residential properties to ensure compliance with State of Illinois tax laws. The solution helped recapture more than $26 million in lost revenue for Chicago and the rest of Cook County, Illinois. Over a period of 4 years, LexisNexis Risk Solutions helped the county bill more than $45 million in lost revenue.

The LexisNexis Homestead Exemption Fraud Detection Solution has also helped the Harris County Appraisal District in Texas save more than $20 million in tax revenue, returning would-be lost money to the jurisdictions’ tax roll. In just the first 18 months of use, the LexisNexis Homestead Exemption Fraud Detection Solution found $21million in erroneous homestead exemption filings across Houston and other locales in the county. The technology has been an integral component of Harris County Appraisal District’s ongoing efforts to improve the auditing process and ensure the integrity of its homestead exemption program, which can lower qualifying homeowners’ property taxes.

Rule of tax law in Africa

Support of SDG 16 through continued advancement of African tax law codification pilots and African Tax Legislation Atlas

Taxes provide governments with the essential revenue necessary for public services that benefit their citizens. Governments need codified tax laws to know when, how much and from whom they should be collecting. Citizens need codified and transparent tax laws to understand their liabilities and to advocate for fair collection and use of their remittances. Unfortunately, in many countries around the world, it is difficult for tax authorities and taxpayers alike to access tax law in a complete, up-to-date and consolidated form.

Taxes provide governments with the essential revenue necessary for public services that benefit their citizens. Governments need codified tax laws to know when, how much and from whom they should be collecting. Citizens need codified and transparent tax laws to understand their liabilities and to advocate for fair collection and use of their remittances. Unfortunately, in many countries around the world, it is difficult for tax authorities and taxpayers alike to access tax law in a complete, up-to-date and consolidated form.

Over the course of three years, the LexisNexis Rule of Law Foundation, LexisNexis South Africa and the tax team at RELX worked on a pro bono basis with Ethiopia’s government to translate that country’s tax laws from Amharic into English, to consolidate those tax laws in both English and Amharic, and to ensure that for the first time they are published and freely accessible on the websites of the Ethiopian Ministry of Finance, Ministry of Revenue, and Customs Commission.

The consolidated tax laws can now be accessed at www.mofed.gov.et (under ‘Resources’ and ‘Consolidated tax laws’), making an important contribution to Ethiopia’s economic development.

“When the project was started, it was based on three main objectives: improving accessibility, transparency and efficiency. The fact that the tax laws are translated and organised in English and made accessible to the user on the website is of great importance to the efforts of Ethiopia to accelerate its growth and development according to the macroeconomic reform and to become a member of the World Trade Organization.” - The Honourable Dr Eyob Tekalign, State Minister of Fiscal Policy and Public Finance, Ethiopia Ministry of Finance.

“When the project was started, it was based on three main objectives: improving accessibility, transparency and efficiency. The fact that the tax laws are translated and organised in English and made accessible to the user on the website is of great importance to the efforts of Ethiopia to accelerate its growth and development according to the macroeconomic reform and to become a member of the World Trade Organization.” - The Honourable Dr Eyob Tekalign, State Minister of Fiscal Policy and Public Finance, Ethiopia Ministry of Finance.

Further to the successful completion of the pilot in Ethiopia, the RELX team are currently in discussion with Kenya’s government to commence a similar project.

The Ethiopia tax law project attracted the attention of the World Bank which has now embarked on an African Tax Legislation Atlas (ATLA) project, a partnership between the World Bank, LexisNexis Rule of Law Foundation and the IBFD, to build an innovative digital repository consolidating Africa’s tax laws to support transparency, comparative analysis and legal reform. The ATLA was initiated in November 2025 with several pilot countries including Ethiopia and Kenya.

Enhancing responsible tax practices (RTP) in Africa

RELX Tax was selected as a responsible tax champion in the RTP project, an initiative of the International Finance Corporation (IFC), a member of the World Bank Group, and the B Team, to enhance responsible tax practices in Africa. This groundbreaking initiative brings together responsible tax leaders and their private sector peers to explore the what, why, and how of responsible tax practices. The project kicked off with a roundtable in Nairobi in April 2025. As a responsible tax champion, RELX has had an opportunity to share our insights and experience of implementing responsible tax practices over the last decade with participant companies from across Africa.

RELX Tax was selected as a responsible tax champion in the RTP project, an initiative of the International Finance Corporation (IFC), a member of the World Bank Group, and the B Team, to enhance responsible tax practices in Africa. This groundbreaking initiative brings together responsible tax leaders and their private sector peers to explore the what, why, and how of responsible tax practices. The project kicked off with a roundtable in Nairobi in April 2025. As a responsible tax champion, RELX has had an opportunity to share our insights and experience of implementing responsible tax practices over the last decade with participant companies from across Africa.